By Rob Miller

Forensic accountant and expert witness specialising in offering expertise on POCA, cryptocurrency, and financial dispute matters.

Updated May 2026 | 11 min read time

Wondering how to calculate the share value of a private company? Valuing shares in a private company is more complex than checking a stock price. Without a public market, there’s no ticker to reference. You need to apply valuation methodologies that account for financial performance, industry conditions, and the specific circumstances of the transaction.

Whether you need a share valuation for a shareholder dispute, divorce settlement, tax purposes, or exit planning, understanding how to calculate share value accurately is vital. Get it wrong and you could pay too much, sell for too little, or face a challenge from HMRC.

As a forensic accountant, I regularly calculate share values for business owners, shareholders, and their professional advisers. This guide explains the methods I use in practice, the factors that affect what shares are actually worth, and when you should instruct a professional.

Rob Miller is a forensic accountant and director of Inquesta Forensic. He provides share valuations, expert witness services, and forensic accounting support for solicitors, business owners, and their professional advisers across England and Wales. Contact Rob directly.

What Is Share Value?

Share value is the monetary worth of an individual share in a company. For public companies, this is simply the traded stock price. For private companies, there’s no market price, so the value must be calculated based on the company’s financial position, earnings capacity, or net assets.

The value depends on two things:

- What the company as a whole is worth.

- How many shares exist.

But it also depends on what proportion of the company the shareholding represents. For example, a 51% controlling stake will naturally be worth more proportionally than a 10% minority holding.

The Share Value Formula

At its simplest, share value is calculated by dividing the total company value by the number of shares in issue: :

Share Value = Company Value ÷ Number of Shares in Issue

For example, if a business is valued at £1,000,000 and has 100,000 shares in issue, each share would be worth £10.

The challenge lies in determining what the company’s value is. Unlike public companies with market capitalisation figures, private companies require valuation using one or more established methodologies.

Share Valuation Methods for Private Companies

There are four main approaches when valuing a private company in the UK. Earnings multiple, net asset value, comparable company analysis, and discounted cash flow. The most appropriate method depends on the nature of the business, the purpose of the valuation, and the available financial information:

1. Earnings Multiple (P/E) Method

This is the most common approach for profitable trading businesses. The company’s maintainable earnings are multiplied by an appropriate price/earnings (P/E) multiple.

The formula:

Company Value = Maintainable Earnings × P/E Multiple

Example: If a company has maintainable earnings of £200,000 and a P/E multiple of 5 is applied, the company value is £1,000,000.

The key questions:

- What are the “maintainable” earnings? Adjustments are made for one-off items, excessive director remuneration, and non-commercial transactions. Raw profit figures rarely represent sustainable earnings.

- What multiple is appropriate? This depends on industry, company size, growth prospects, and risk profile. Multiples for private companies typically range from 3-8x. This is significantly lower than listed companies due to lack of liquidity and higher risk.

In my experience, disputes often arise because parties disagree on what multiple is appropriate. Small differences have significant effects on the final figure.

2. Net Asset Value (NAV) Method

This approach values the company based on its net assets: total assets minus total liabilities.

The formula:

Company Value = Total Assets − Total Liabilities

When I may use this approach:

- Property investment companies.

- Holding companies.

- Asset-rich businesses (manufacturing, plant hire).

- Companies being wound up.

- Loss-making businesses where earnings methods produce nil or negative values.

Assets may be valued at book value or adjusted to market value depending on circumstances. Property especially often needs professional revaluation. An asset’s book values rarely reflect current market prices.

3. Comparable Company Analysis

Where transaction data is available, benchmarking against similar businesses that have sold can provide useful context.

The approach:

- Identify comparable transactions. Businesses in the same sector, of similar size, sold in recent years

- Calculate the multiples achieved. This typically refers to EV/EBITDA or price/revenue ratios.

- Apply relevant multiples to your company, adjusting for significant differences.

The limitation: Private company transaction data is often scarce. Unlike public markets, there’s no comprehensive database of every deal. This method typically works better as a cross-check than a standalone calculation.

4. Discounted Cash Flow (DCF)

DCF values a business based on projected future cash flows, discounted back to present value.

When it’s used:

- High-growth companies where historic earnings don’t reflect future potential.

- Businesses with significant expected changes in profitability.

- As a cross-check against other methods.

The drawback: DCF relies heavily on assumptions about future growth rates and discount factors. Small changes in inputs produce large swings in output. I typically use it to supplement other methods rather than as a primary approach.

Which Method Should You Use?

| Business Type | Recommended Method | Why |

| Trading company with stable profits | Earnings multiple | Value lies in ongoing profit generation. |

| Property or investment company | Net asset value | Asset backing is the primary value drive. |

| Loss-making business | Net asset value | Earnings method would produce nil/negative. |

| High-growth company | DCF or comparables | Historic earnings don’t reflect potential. |

| Professional services firm | Earnings multiple | Possibly with separate goodwill adjustment. |

In practice, I often calculate value using multiple methods and compare results. If they diverge significantly, that tells me something important about the business that warrants further investigation.

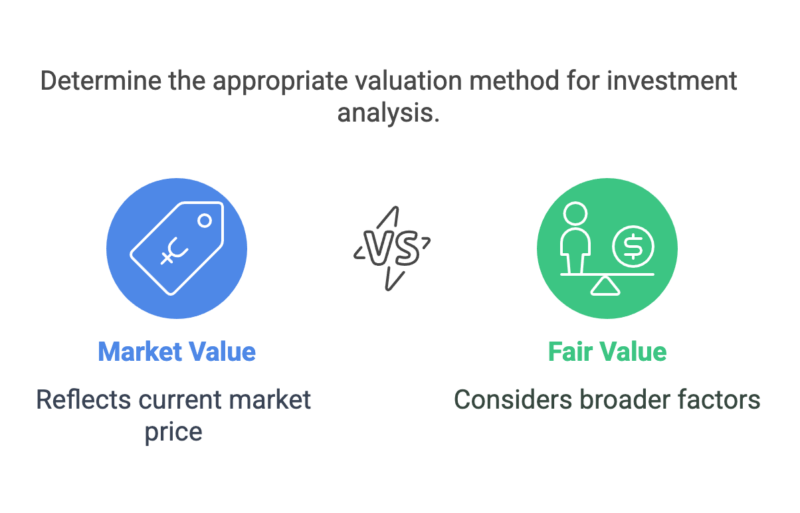

What is ‘Fair Value of Shares’?

The fair value of shares is the price that would be agreed between a willing buyer and seller, both acting with full knowledge and neither under pressure to transact. It accounts for the specific circumstances of the transaction. Not just theoretical market conditions.

When calculating fair value, I first check the company’s articles of association. These documents sometimes define what constitutes “fair value” for internal transfers — though this isn’t always the case.

Fair value is particularly relevant in shareholder disputes where parties disagree on what shares are worth. In such circumstances, the fair value figure will be determined by what factors your valuer (or the court) considers important.

Market Value vs Fair Value of Shares

Understanding the difference between market value and fair value is crucial when learning how to calculate the share value of a private company. These two approaches to private company valuation are distinct:

- Market Value: Reflects the price a buyer would pay in a competitive and open market. For example, if a similar company in the same industry sold shares for £100 each, this could influence the market value of your shares.

- Fair Value: Takes into account broader factors, such as minority shareholders’ rights and restrictions. For instance, shares with limited voting rights may be deemed less valuable, even if their market value suggests otherwise.

Understanding these differences is essential for accurately valuing shares in a private company.

| Market Value | Fair Value | |

| Definition | Price achievable in open market. | Price agreed between specific parties. |

| Discounts | Typically includes minority/marketability discounts. | May or may not, depending on purpose. |

| Common use | Business sales, investment rounds

. |

Internal transfers, disputes, tax. |

Getting the basis wrong can have significant consequences — particularly with HMRC or in court proceedings.

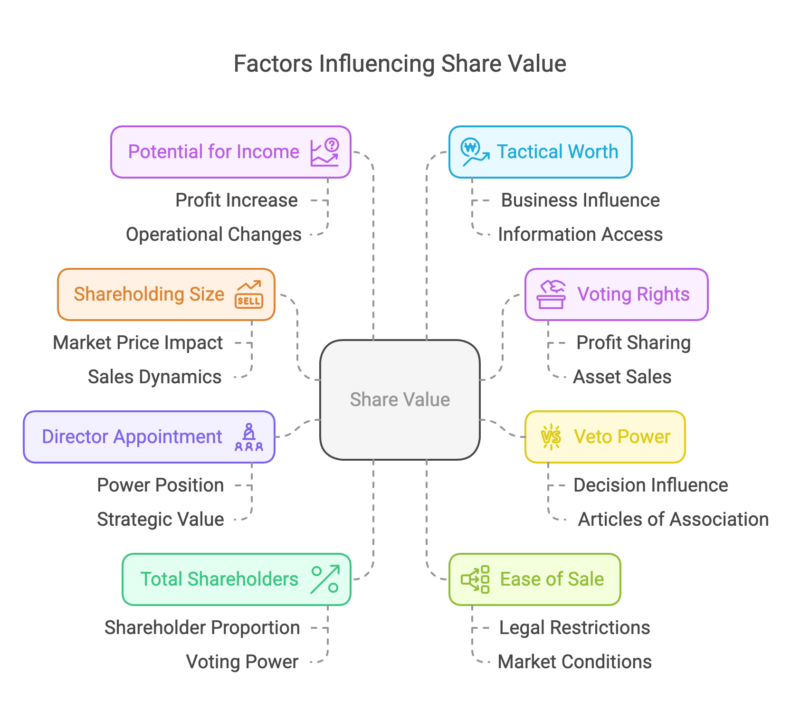

Factors That Affect Share Value

Calculating company value is only part of the picture. Several factors affect what a specific shareholding is actually worth:

Size of Shareholding

The percentage you own determines your level of control — and control has value.

| Shareholding | Rights | Value Implication |

| 75%+ | Can pass special resolutions. | Premium for control. |

| 51-74% | Ordinary control. | Control premium applies. |

| 25-50% | Can block special resolutions. | Some strategic value, but discount applies. |

| Under 25% | Limited influence. | Significant minority discount (10-50%). |

Voting Rights

Shares with enhanced voting rights are inherently more valuable than restricted or non-voting shares. Voting rights affect your ability to influence key decisions such as profit distribution and asset sales.

Veto Powers

Depending on the articles of association, shareholders with 25% or more of total shares may have the power to veto special resolutions. This blocking power has value even without majority control.

Right to Appoint a Director

The ability to appoint a director puts a shareholder in a more powerful position. Board representation means influence over company strategy and operations.

Shareholder Composition

Being a 10% shareholder carries more weight if nine others also own 10% each (everyone has equal say) than if two others own the remaining 90%. The proportional makeup affects your practical influence.

Restrictions on Transfer

Articles of association often restrict how shares can be transferred. This includes pre-emption rights, director approval requirements, or prohibitions on external sales. A share you cannot freely sell is worth less than one you can.

Potential for Income

Expected increases in profits, either from new services, operational changes, or market growth, can significantly boost share value.

Tactical Worth

Even a minority shareholding can influence a company’s future or provide access to strategically important information. The greater a share’s influence and access, the more valuable it becomes.

Common Mistakes When Calculating Share Value

Having valued shares in many different contexts, I regularly see the same errors:

- Using Outdated Financial Information: A valuation based on accounts that are two years old won’t reflect current trading.

- Failing to Adjust Maintainable Earnings: One-off costs, exceptional income, above-market owner salaries, and non-recurring items all need adjustment.

- Applying Inappropriate Multiples: Using a multiple from a different sector or company size will skew results. Private company multiples (3-8x) are significantly lower than public company equivalents.

- Ignoring Minority/Marketability Discounts: A 20% shareholding is not worth 20% of total company value.

- Relying on a Single Method: Different approaches suit different businesses. Using multiple methods and comparing results will give significantly more reliable outcomes.

What Information Is Needed?

When I’m instructed to calculate share value, I typically need:

Financial information:

- Statutory accounts for the past 3-5 years.

- Management accounts for the current period.

- Forecasts and budgets where available.

- Details of exceptional or non-recurring items.

Corporate documents:

- Articles of association.

- Shareholders’ agreement if one exists.

- Details of share classes and rights.

Business context:

- Customer concentration and key contracts.

- Market position and competitive landscape.

- Key personnel dependencies.

- Significant assets, particularly property.

Frequently Asked Questions

What is Share Valuation?

Share valuation is the process of determining what a share in a company is worth. For private companies, this involves analysing financial data, selecting appropriate valuation methods, and making adjustments for factors like minority shareholdings and transfer restrictions.

How Much are my Shares Worth?

The value depends on overall company value, how many shares exist, and the specific rights attached to your shares. Calculate company value using earnings multiple or net asset methods, divide by total shares, then apply any relevant minority or marketability discounts.

How do I Calculate how Much my Shares are Worth?

Start with the formula: Share Value = Company Value ÷ Number of Shares. For trading businesses, use maintainable earnings × an appropriate multiple (typically 3-8x for private companies).

For property companies, use net asset value. Then consider discounts for minority holdings or transfer restrictions.

What is the Best Way to Value a Private Company?

There’s no single “best” method. It depends solely on the business. Earnings-based valuation suits profitable trading companies. Asset-based valuation suits property or investment businesses. Using multiple methods and comparing results gives the most reliable indication.

Can I Calculate Share Value Without Professional Help?

For rough estimates and internal planning, yes. The methods highlighted in this guide can give you a reasonable indication. However, for anything involving HMRC, legal proceedings, or third-party transactions, professional valuation is advisable.

When Do You Need Professional Help?

For informal purposes, getting a rough sense of what shares might be worth, the methods above can provide a reasonable estimate. However, for anything involving third parties, tax authorities, or legal proceedings, professional valuation becomes important:

- Tax Submissions: HMRC’s Shares and Assets Valuation team reviews share valuations and may challenge unreasonable figures.

- Shareholder Disputes: Courts expect robust, independent valuations supported by clear methodology.

- Share Transfers and Buyouts: Both parties typically want independent confirmation of fair value.

- Employee Share Schemes: EMI and other schemes require defensible valuations.

- Inheritance and Restructuring: Valuations are often required for probate, estate planning, or company reorganisations.

A professional valuation provides independence, technical rigour, and experience of how valuations are scrutinised in contested situations.

Need Help Calculating the Share Value of a Private Company?

If you need to calculate the share value of a private company, whether for tax purposes, a share transfer, resolving a dispute, or exit planning, I can help.

I provide independent share valuations that are technically robust and, where required, capable of withstanding scrutiny from HMRC or in court proceedings. I work with business owners, solicitors, and other professional advisers across England and Wales.

If you’re unsure whether you need a formal valuation or just want to talk through your situation, feel free to get in touch for an initial conversation.

Contact Inquesta Forensic today to discuss your requirements and receive personal, specialist support.